Life Insurance 101

This video will help you see when getting life insurance is smart and when it’s not. I also include a screen share of insurance shopping and figuring out how much you need, if you need it. Life insurance agents are highly compensated based on commissions they receive, so they are pretty skilled at making you […]

This video will help you see when getting life insurance is smart and when it’s not. I also include a screen share of insurance shopping and figuring out how much you need, if you need it.

Life insurance agents are highly compensated based on commissions they receive, so they are pretty skilled at making you feel like you need insurance regardless of your circumstances, so finding someone you trust is really important.

I used to hold a license to sell life insurance, but I am no longer licensed and my knowledge is limited in the subject since it was never a focus of mine. Keeping that in mind, this video is designed to give you some perspective and things to consider with life insurance so you can ask good questions and run numbers to see if you are getting the best policy for your situation.

Life insurance is a very sensitive subject because it’s unbearable thinking about the possibility of our partner dying. I also really believe in the law of attraction and manifesting, so I know that thinking about this or even purchasing life insurance can feel like we are attracting this bad energy, but in reality, we aren’t it’s just taking the precaution because we are not immortal and if something does happen then this allows our loved one the space to heal without worrying about the bills. We have auto insurance and health insurance and that isn’t us attracting the potential for an accident or health problems, it’s just being a responsible person.

That being said, as I am creating this video, we only have one year worth of insurance for my husband that is offered through his work, but creating this video has made me think about all of this and we are in considering getting term life insurance, but more on that later.

Life insurance is meant to offer a source of financial security for your dependents if you were to pass away.

A dependent is anyone that counts on you for their financial support. A spouse and children are the first to consider. If your income were to be taken out of the equation for your family, how long could the bills be paid? If your spouse brings in enough income to take care of all of the financial obligations and additional obligations that will arise with your contribution of time/energy missing, then you don’t need life insurance, but you may still want it.

If your income covers a certain percentage of the bills, then it would be really helpful for your spouse and children if you at least got enough life insurance to cover that portion of the annual expenses.

A lot of people have some coverage from work and they may feel like that is enough. Typically you get one year’s salary included in your benefits, that may seem like a lot if you just consider receiving a lump sum, but in reality, it will only cover one year worth of expenses for your family if you typically use the majority or all of your annual salary. That’s where purchasing additional insurance to go with what’s included can be helpful.

When is life insurance not important. When you have no one depending on you for your income. If this is you, then you still can get it as a gift to your parents, family, or anyone really, but you may want to focus on other financial goals first.

Now let’s get into different options. Remember that my knowledge around this is very general. You will get the basic idea of this, not the full scope.

Term and Permanent

Term is the cheapest and best option IMO. With term life insurance, you figure out how much money your dependents will need and for how long. I found this great resource on NerdWallet’s site that is super easy and helpful. I share the tutorial on the associated video.

Now let’s discuss what whole or permanent insurance is.

Whole life insurance is designed to cover your whole life. Anytime you die, even at age 80, your beneficiaries will receive your coverage amount. People like the idea of this because it may feel like term insurance is just throwing money away since it’s as if you never had it after the set term expires, but with whole life you still have your benefit. There is a hefty price to pay for this coverage and you may do better just investing the difference between term life and the whole life premium.

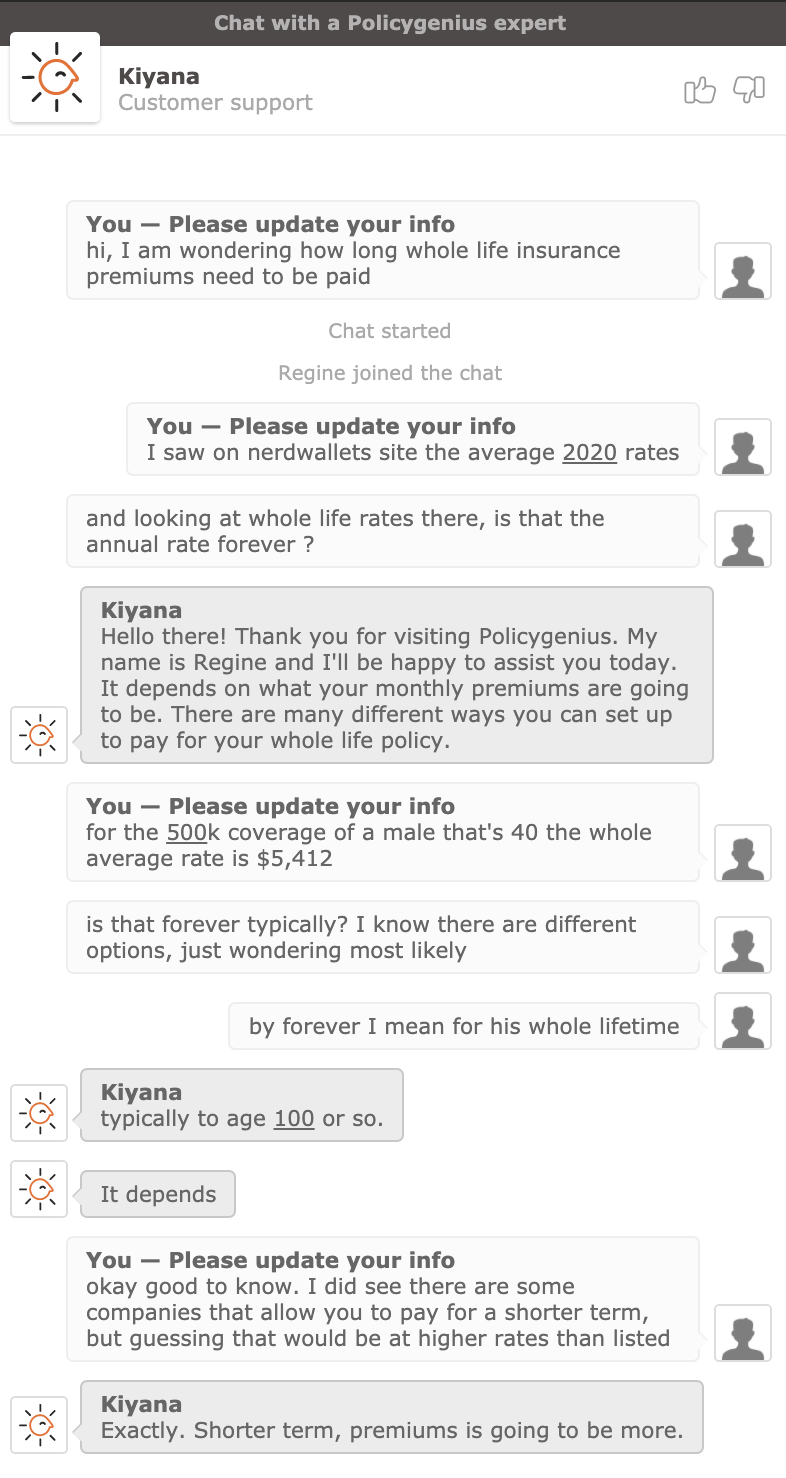

Let’s break down the numbers. Using this chart with 2020 average rates I will show you how it looks to invest the difference.

I am just going to use our numbers, so you can see the exact work we are doing. You can use the same calculations for your specifics. Links below (avg. rates: https://www.nerdwallet.com/blog/life-insurance/ )

My husband is 42 and I feel comfortable with $500k of coverage. This is below the recommended amount for us, but taking into consideration what we already have saved up and my ability to invest the premium to make it last for a long time, I feel secure with this coverage. On the subject of investing, that’s primarily what I cover on my channel, so subscribe and take a look at other videos if investing is interesting to you.

Alright, crunching numbers time:

For a 20-year term policy, it would cost us $341/ year or about $28/month. A whole life policy would cost us $5,412/year or $451/month. First I had to figure out how long these whole life premiums needed to be paid, so I chatted with someone from the customer support of Policy genius which is who nerd wallet links to for resources. They said that premiums are typically paid until the person covered reaches 100! Unless I am misunderstanding something- that’s a lot of money over a long period of time.

We’ll start by taking the term rate out of the whole rate so we can then see what it would look like to invest the difference vs keeping it in the policy. So 451-28=423 this is what we will enter in the calculator first for 20 years then for 60 years which would be 100-40=60. we will use a rate of return of 10% which is what the S&P has returned over the long term historically.

Over a 20 year timeframe with 423 invested monthly, it is likely to grow to about $321k which doesn’t cover the 500k, but after 25 years you cross over that 500k investing on your own. For a situation like this, I would run the numbers and see where the break-even is and perhaps get a few years extra term coverage to be safe. This allows you to have the coverage needed and then you have full access to the extra money you have invested over time. Your money is likely to grow much more than it would in the whole policy.

Dave Ramsey gives some great breakdowns on life insurance, so I will link some of his articles below.

“Cost Comparison of Life Insurance by Dave Ramsey” https://www.daveramsey.com/blog/term-life-vs-whole-life-insurance

To sum things up, run your numbers and see what you need. If you can’t afford the premiums for term, then take a look at a lower amount. Something will be better than nothing. For us, it’s recommended that we have $2MM in coverage, but that doesn’t account for my ability to invest, make money on my own to cover the difference, and my own comfort level of what we actually need, which is why I can to $500k worth of coverage for us

Ready to find the right life insurance policy for your needs? This Life Insurance article provides you in-depth information on what to know, pros & cons, and comparison on companies so you can shop around and evaluate which can offer you the best option for you and your family.

Resources for notes:

How much do I need:

Compare Quotes

need help investing?

Let's Get Started Investing, Together.

Browse my best selling courses to get a solid foundation on how to start investing and preparing for your future!

")

PLEASE COMMENT BELOW